核心要点

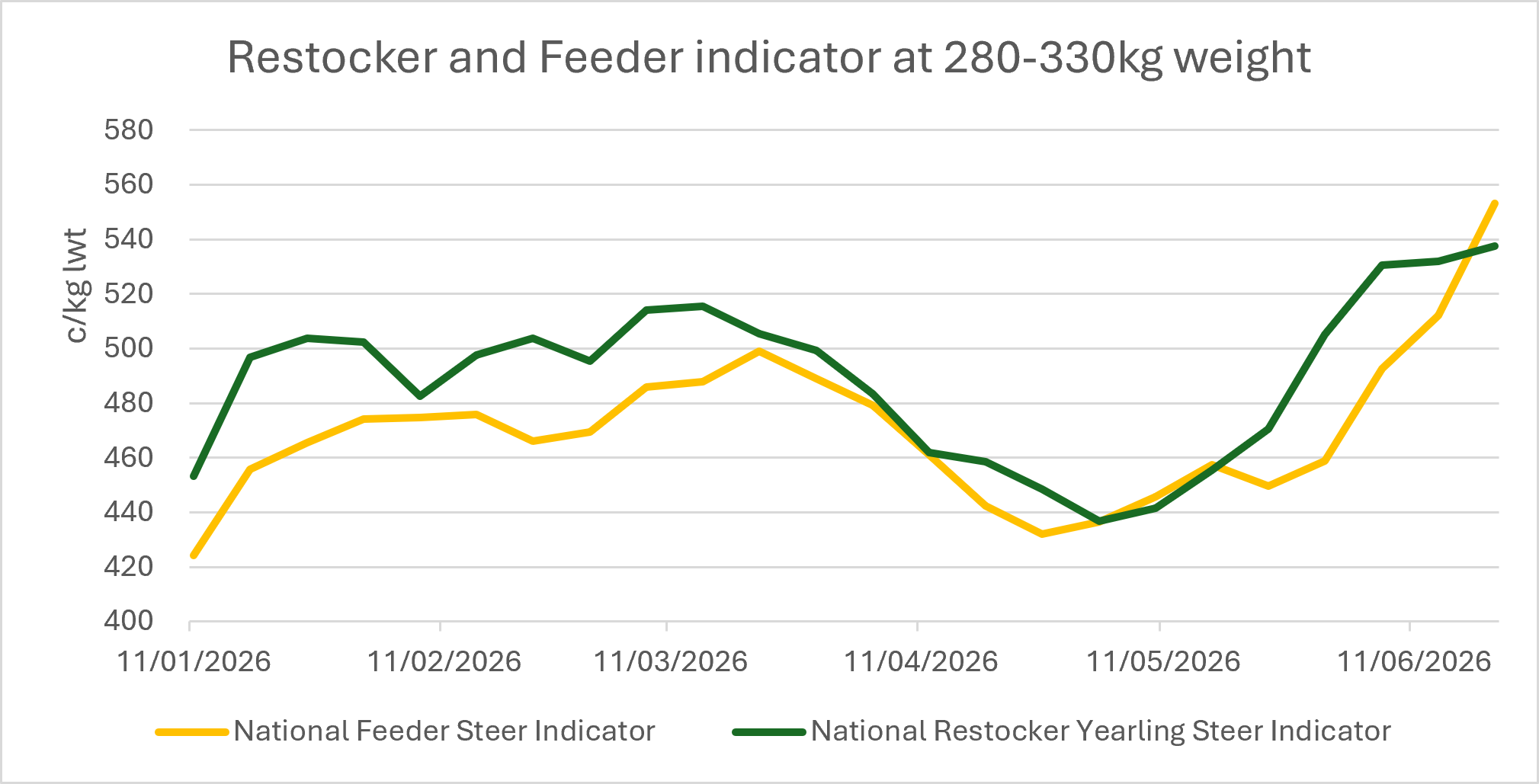

自4月以来,草场补栏用一岁阉牛每公斤活重涨幅接近100澳分,育肥用阉牛每公斤活重涨幅超70澳分。

草场补栏一岁阉牛价格持续高于育肥阉牛,草场养殖户与谷物育肥场争夺同批次牛源。

280至400公斤区间牛只竞争最为激烈,昆士兰州供货量充足,新南威尔士州主导价格上行。

草场补栏养殖户持续拉动整体肉牛市场,前期育肥散户与规模化育肥场竞争加剧,双方争抢供给收紧的青年牛源。

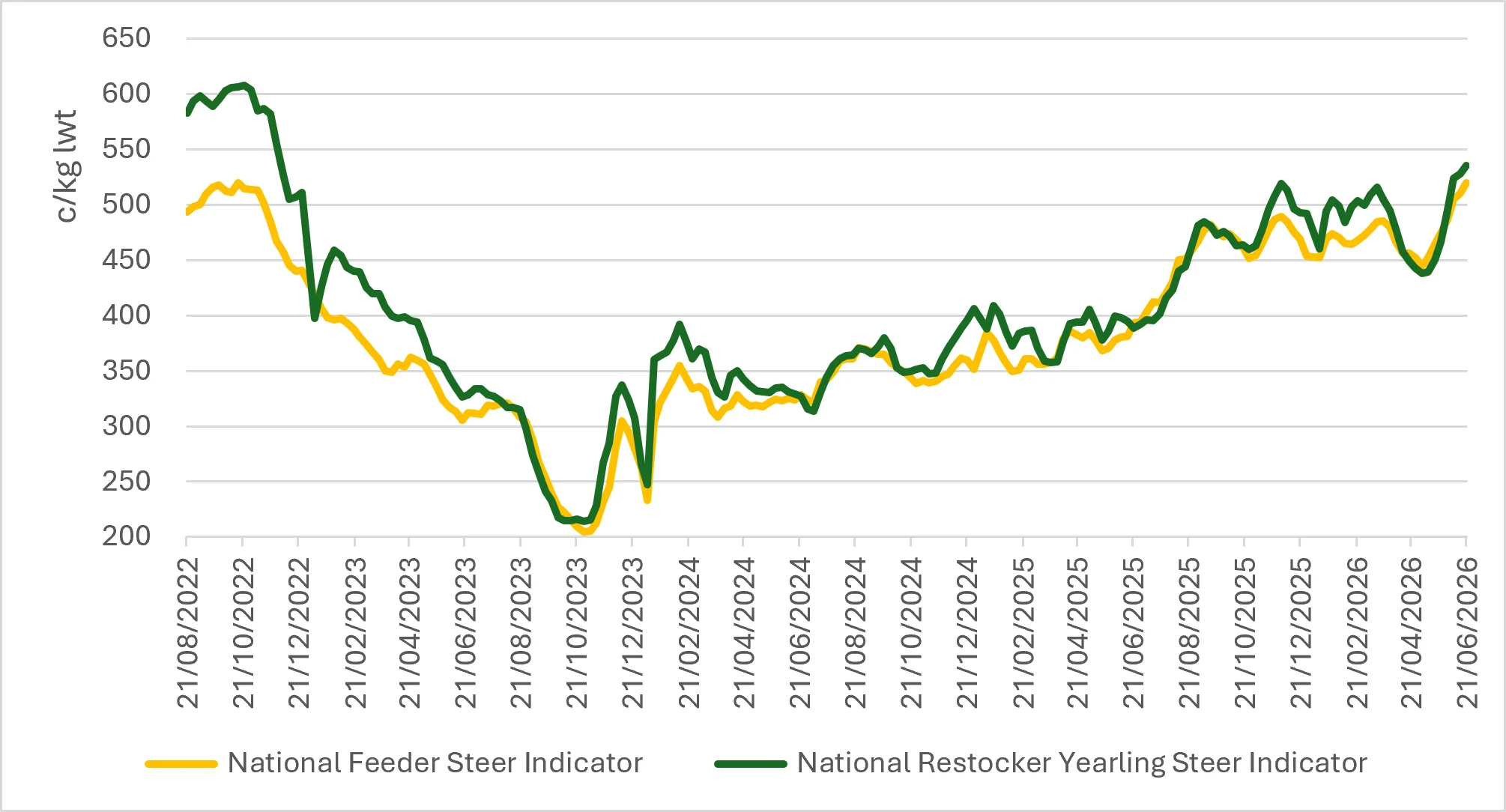

全国育肥阉牛指数上涨25澳分,报530澳分/公斤活重;全国补栏一岁阉牛指数上涨3澳分,同样报530澳分/公斤活重。两类牛价双双突破本月上旬前期高点,创下2022年以来新高。

补栏一岁阉牛依旧保持对育肥阉牛的溢价,价差约15澳分/公斤活重。育肥场持续稳固市场底价,但当前行情由补栏养殖户主导,在农户对气候长势预期向好的地区表现尤为突出。

4月末至今,草场补栏一岁阉牛每公斤活重大幅上涨100澳分,育肥阉牛同步上涨94澳分/公斤活重4月时干旱天气、上市牛只数量偏多打击补栏养殖户采购信心,当前市场行情已出现明显反转。

此前市场行情由育肥场主导,如今草场养殖户与谷物育肥场争抢同一批阉牛,市场竞争加剧。育肥场因持续有谷饲肉牛出栏需求,采购需求保持坚挺;而补栏需求回暖,进一步加快牛价回升速度。

体重区间竞争

从牛只体重分布可清晰看出市场竞争激烈区间。育肥场采购需求集中在大体重牛只,重点为330–400公斤及400公斤以上牛群。本周该体重段阉牛交易量占育肥牛总量大头,说明育肥场仍优先选择可快速转入谷饲育肥流程的牛只。

但中小体重育肥牛价格同步走高,反映采购方开始向下争夺货源紧缺的轻量级牛只。280–330公斤育肥牛本周涨幅居前,即便上市总量偏少。这意味着育肥场正主动争抢原本更受草场补栏户青睐的牛源。

草场补栏需求均匀覆盖200–400公斤区间,其中200–280公斤上市量最大。330–400公斤补栏牛价格同样坚挺,为所有补栏体重段均价最高。可见补栏养殖户不仅收购小型牛只回草场放牧,也愿意与育肥场竞争增重空间更大的大体重一岁牛。

280至400公斤体重区间是两类采购群体争夺最激烈的重叠区间。该体重段牛只可根据骨架、膘情、饲草供给及收购利润,选择草场放牧或谷饲育肥两种养殖路径。草场补栏牛价格持续高于育肥牛,说明当前前期育肥养殖户愿意出高于育肥场的价格收购优质牛源。

昆士兰州保障牛只供给,新南威尔士州拉动价格上涨

昆士兰州持续供应大量牛只,主要集中在罗马、布莱科尔、多尔比与格雷斯米尔交易市场。本周草场补栏一岁阉牛交易中,罗马市场供货量占总量三分之一以上,成交均价高于全国均值;布莱科尔市场上市量虽有所减少,但价格上行,同样提振整体指数。

罗马、布莱科尔市场成交行情向好,加之沃加市场高价牛只成交,共同推高草场补栏牛价格指数。

育肥阉牛货源主要依靠昆士兰州,但价格上涨动力多来自新南威尔士州。布莱科尔、多尔比、罗马为育肥牛主要供货市场,沃加、卡库尔、冈尼达与塔姆沃思成交均价均远超全国平均水平。其中冈尼达、卡库尔周度涨幅领跑,沃加市场则同步实现供货量与成交价双重走高。

撰稿:澳大利亚肉类及畜牧业协会高级市场信息分析师 埃米利亚诺・迪亚斯

数据截至2026年6月17日撰稿当日

澳大利亚肉类及畜牧业协会(MLA)不对本刊物所载任何信息的准确性、完整性及时效性作出任何保证。用户使用或依赖本刊物任何内容,风险自行承担;因使用或依赖相关信息所造成的任何损失与损害,MLA概不承担任何责任。未经MLA事先书面许可,本刊物任何内容不得擅自转载、复制。凡使用MLA刊物、报告及相关信息,均须遵守MLA市场报告及信息使用条款。

消息来源:MLA

Restockers challenge feedlots for young steer supply

Key points

Restocker yearling steers have lifted close to 100¢/kg lwt, while feeder steers have gained more than 70¢/kg lwt since April.

Restocker yearling steers maintained a premium over feeder steers as grass and grain buyers competed for the same cattle.

Competition is strongest across the 280–400kg range, with Queensland providing volume and NSW driving much of the price strength.

Restockers continue to drive the overall cattle market due to strong competition between backgrounders and feedlots, with both buyer groups competing for a tighter supply of young cattle.

The National Feeder Steer Indicator lifted 25¢ to 530¢/kg liveweight (lwt), while the National Restocker Yearling Steer Indicator rose 3¢ to 530¢/kg lwt. They both overcame the recent peak earlier this month and set a new high (since 2022).

The move kept restocker yearling steers at a premium to feeder steers, with the spread sitting around 15¢/kg lwt. Feedlots continue to provide a firm price floor, but restockers are now setting the pace, particularly where seasonal confidence has improved.

Since late April, restocker yearling steers have gained a significant 100¢/kg lwt, while feeder steers have also lifted 94¢/kg lwt. This marks a clear shift from April, when dry conditions and larger offerings weighed on restocker confidence.

The market has moved from a feeder-led base to a more competitive environment where grass and grain buyers are bidding into the same steer pool. Feedlot demand remains firm, supported by ongoing grainfed turn-off requirements, but the return of restocker demand has accelerated the price recovery.

Weight range competition

The weight profile shows where competition is strongest. Feeder demand remains concentrated in heavier lines, particularly 330–400kg and 400kg-plus cattle. These weights accounted for most feeder steer throughput this week, confirming feedlots are still focused on cattle that can move efficiently into grain programs.

However, the lift in lighter feeder categories suggests buyers are reaching further down the weight range where supply is tight. The 280–330kg feeder segment recorded one of the strongest weekly price movements, albeit off a smaller offering. This points to feedlot buyers competing more actively for cattle that would otherwise have attracted restocker interest.

Restocker demand was more evenly spread across 200–400kg cattle, with the strongest volume in the 200–280kg range. The 330–400kg restocker category also held firm, trading at the highest average price across the restocker weight ranges. This demonstrates that restockers are not only chasing lighter cattle to put back on grass but are also prepared to compete for heavier yearlings with more production flexibility.

The overlap is most evident in the 280–400kg range. These cattle can suit either pathway depending on frame, condition, feed availability and buyer margins. Restocker values holding above feeder values suggest backgrounders are currently prepared to outbid feedlots for the right animal.

Queensland supplies the numbers, while NSW drives price momentum

Queensland continued to provide the volume base, particularly through Roma, Blackall, Dalby and Gracemere. In the restocker yearling steer market, Roma was the dominant contributor this week, accounting for more than one-third of throughput and trading above the national average. Blackall also supported the indicator, with prices lifting despite a smaller yarding.

The restocker indicator was supported by stronger results through Roma and Blackall, alongside high-priced lines at Wagga.

For feeder steers, Queensland supplied depth, but NSW provided much of the price strength. Blackall, Dalby and Roma were the largest volume contributors, while Wagga, Carcoar, Gunnedah and Tamworth all traded well above the national average. Gunnedah and Carcoar recorded some of the strongest week-on-week price improvements, while Wagga added both volume and price support.

Attribute content to: Emiliano Diaz, MLA Senior Market Information Analyst.

Information is correct at time of writing on 17 June 2026.

MLA makes no representations as to the accuracy, completeness or currency of any information contained in this publication. Your use of, or reliance on, any content is entirely at your own risk and MLA accepts no liability for any losses or damages incurred by you as a result of that use or reliance. No part of this publication may be reproduced without the prior written consent of MLA. All use of MLA publications, reports and information is subject to MLA’s Market Report and Information Terms of Use.

Source:MLA