核心要点

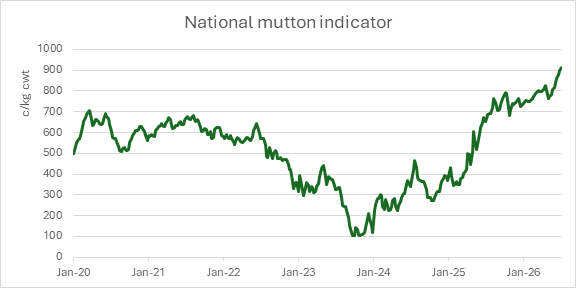

全国羊肉参考价首次突破每公斤活重900澳分。

此前三年持续大量出栏,造成当前供应紧缺。

加工厂竞相采购数量大幅缩减的可屠宰羊群。

本周国内羊肉市场再创新高,全国羊肉参考价升至胴体重量每公斤928澳分。自2025年下半年起羊肉价格便处于历史高位,本次指标首次突破胴体重每公斤900澳分,延续冬季以来的大幅涨价态势。

来源:澳大利亚国家活畜资源信息局(NLRS)

此次涨价反映出市场可售羊群数量持续不足,采购商竞争激烈。羔羊肉价格同样处于历史高位,而羊肉更是肉羊行业当前供应紧张最直观的体现。与此同时,经过数年肉羊大量出栏后,屠宰加工产能有所扩张。

因此,大体重羊、育肥优良母羊及适配加工厂的批次货源竞争最为激烈。上周瓦加牲畜市场,一批大体重母羊拍出单头最高396澳元的价格,足见成品羊肉需求旺盛。

清群出栏带来的影响

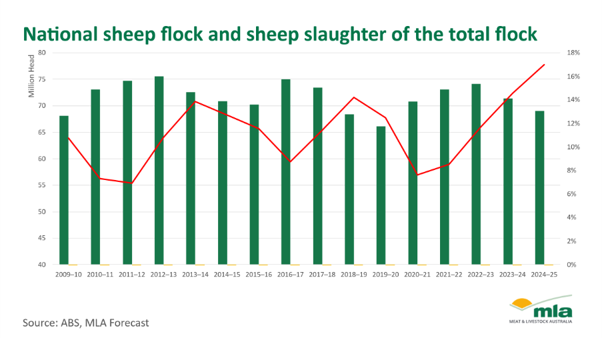

创纪录高价的核心诱因是肉羊供给减少。2023、2024、2025连续三年大规模清群出栏后,市场供应出现短缺;当时南部主产区气候恶劣,饲草不足、养殖户经营信心受挫,纷纷缩减存栏。

这三年是史上肉羊出栏量最高的三个年份,大量肉羊流向市场,直接造成当前可上市肉羊存量锐减。澳洲南部部分地区气候条件好转,养殖户养殖策略随之改变。饲草充足区域的农户选择留存母羊、扩充羊群存栏、暂缓出栏,进一步减少流入牲畜交易市场与屠宰厂的肉羊供应量。

屠宰产能与收购竞争

此前屠宰量高位阶段,加工厂投入资金提升生产效率、扩建厂区。2022年至今,行业通过厂房扩建、人力优化及运营增效,新增约1000万头肉羊屠宰产能。

对比全国存栏总量与屠宰量便能直观看出变化。2022年全国肉羊存栏7300万头,屠宰620万头,占总存栏9%。2025财年屠宰量升至1170万头,占总存栏17%,为近年存栏承压最严重的屠宰规模。

现有屠宰产能是基于此前极高出栏量建设,如今供给大幅收紧。屠宰厂难以收够肉羊维持生产线运转,收购货源竞争愈发激烈。

加工厂已采取缩减班次、延长冬季检修停工时间等应对措施,但供给缩减速度远超屠宰厂调整屠宰计划的速度。澳大利亚国家活畜资源信息局屠宰数据显示,肉羊周屠宰量自2024年12月25.5万头的近期峰值降至上周4.6万头,创2020年7月以来最低。

牲畜交易市场供货量

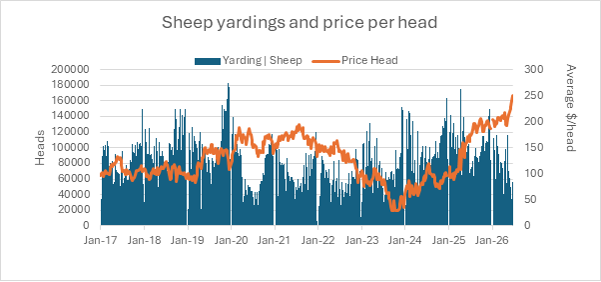

牲畜市场报告显示,各核心交易市场均印证全国整体走势。全国肉羊上市量于2025年4月达到约17.5万头峰值,此后降幅约八成,6月上市量仅3.5万至4.5万头。瓦加市场是全国行情主要代表,羊肉均价接近胴体重每公斤980澳分,部分大体重母羊批次成交价突破胴体重每公斤1000澳分。

来源:澳大利亚国家活畜资源信息局(NLRS)

短期羊肉价格走势或将持续由供应主导。养殖户持续留存母羊、饲草条件改善、牲畜市场上市量不足均会对价格形成支撑。主要利空风险包括屠宰厂屠宰空间缩减、冬季停工检修、肉质品质参差不齐以及海外采购商抵触高价。

信息来源:澳大利亚肉类与畜牧业协会资深市场分析师埃米利亚诺·迪亚兹

信息更新截至2026年7月2日撰稿当日

澳大利亚肉类及畜牧业协会(MLA)不对本刊物所载任何信息的准确性、完整性及时效性作出任何保证。用户使用或依赖本刊物任何内容,风险自行承担;因使用或依赖相关信息所造成的任何损失与损害,MLA概不承担任何责任。未经MLA事先书面许可,本刊物任何内容不得擅自转载、复制。凡使用MLA刊物、报告及相关信息,均须遵守MLA市场报告及信息使用条款。

消息来源:MLA

Why are mutton prices in unprecedented territory?

Key points

The National Mutton Indicator lifted above 900¢/kg cwt for the first time.

Current short supply follows three years of elevated turn-off.

Processors are competing for a much smaller pool of available sheep.

The national mutton market reached new territory this week, with the National Mutton Indicator lifting to 928¢/kg carcase weight (cwt). Mutton prices have been trading at historically high levels since the second half of 2025, but this is the first time the indicator has moved above 900¢/kg cwt, extending the sharp price recovery seen through winter.

Source: NLRS

The lift reflects a market where available sheep numbers remain limited, and buyer competition is firm. While lamb prices have also been historically strong, mutton has become the clearest example of the current supply squeeze across the sheepmeat sector. At the same time, processing capacity has expanded following several years of elevated sheep and lamb turn-off.

As a result, heavy sheep, well-finished ewes and processor-suitable lines are attracting the strongest competition. At Wagga last week, buyers paid up to $396/head for a pen of heavy ewes, highlighting the strength of demand for finished mutton.

The impact of destocking

The key driver of the record price is the reduced availability of sheep. Current short supply follows three years of elevated turn-off in 2023, 2024 and 2025, largely due to destocking across southern production regions as tough seasonal conditions pressured feed availability and producer confidence.

These three years accounted for the three largest sheep supply years on record, with significant numbers moving through the system and reducing the pool of sheep now available to market. Improved seasonal conditions across parts of southern Australia have also changed producer behaviour. Where feed is now available, producers are retaining ewes, rebuilding flock numbers or holding stock rather than selling, further reducing sheep flow into saleyards and processor channels.

Processor capacity and competition

During the recent period of high throughput, processors invested in improve efficiency and expanding facilities. Since 2022, the industry has added an estimated 10 million head of sheep and lamb processing capacity through plant expansion, labour improvements and operational efficiencies.

The change is clear when looking at sheep slaughter relative to the national flock. In 2022, 6.2 million sheep (9% of the total flock) were processed from a flock of 73 million head. By FY2025, 11.7 million sheep were processed, equal to 17% of the flock and the highest slaughter pressure on the flock in recent times.

Current capacity was built around very high throughput, but supply has now tightened sharply. This has created a challenge for processors trying to secure enough sheep to maintain processing chains and has underpinned strong competition for available stock.

Processors have responded by reducing shifts and extending winter maintenance shutdowns. However, supply has reduced faster than the processors’ ability to adjust kill schedules. According to the NLRS slaughter report, sheep processing throughput has fallen from a recent weekly peak of 255,000 head in December 2024 to 46,000 head last week – the lowest level since July 2020.

Saleyard supply

Saleyard reports show the national trend is being reinforced at key selling centres. Sheep yardings peaked in April 2025 at around 175,000 head before falling by about 80% to sit near 35,000–45,000 head in June. Wagga was a major contributor to the national result, with mutton averaging close to 980¢/kg cwt and some heavy ewe lines moving beyond 1,000¢/kg cwt.

Source: NLRS

Near-term mutton prices are likely to remain supply led. Continued ewe retention, improved feed conditions and tight saleyard numbers would keep prices supported. The main downside risks are reduced processor kill space, winter shutdowns, quality variation and price resistance from export customers.

Attribute content to: Emiliano Diaz, MLA Senior Market Information Analyst.

Information is correct at time of writing on 2 July 2026.

MLA makes no representations as to the accuracy, completeness or currency of any information contained in this publication. Your use of, or reliance on, any content is entirely at your own risk and MLA accepts no liability for any losses or damages incurred by you as a result of that use or reliance. No part of this publication may be reproduced without the prior written consent of MLA. All use of MLA publications, reports and information is subject to MLA’s Market Report and Information Terms of Use.

Source:MLA