核心要点

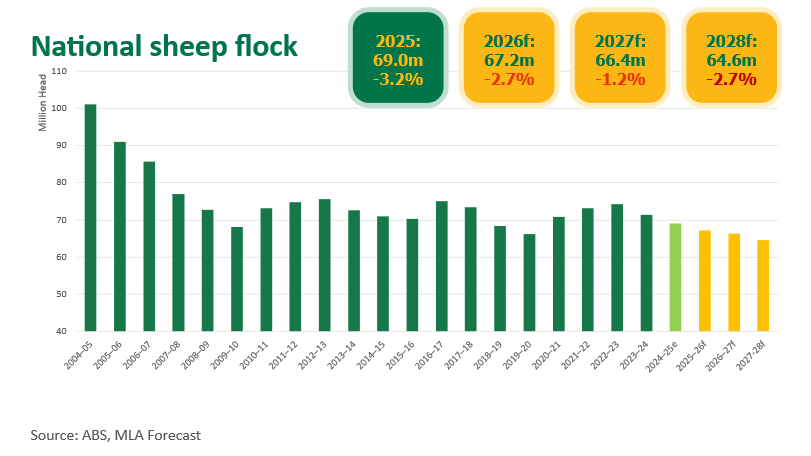

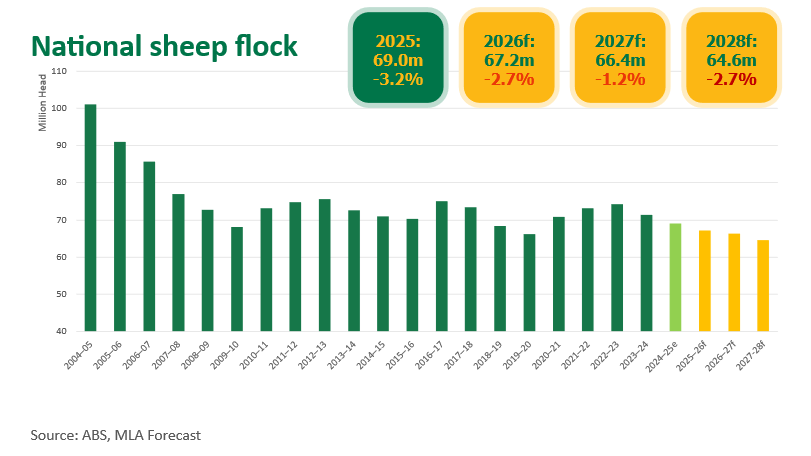

2026 年,全国绵羊存栏量预计降至 6710 万头。

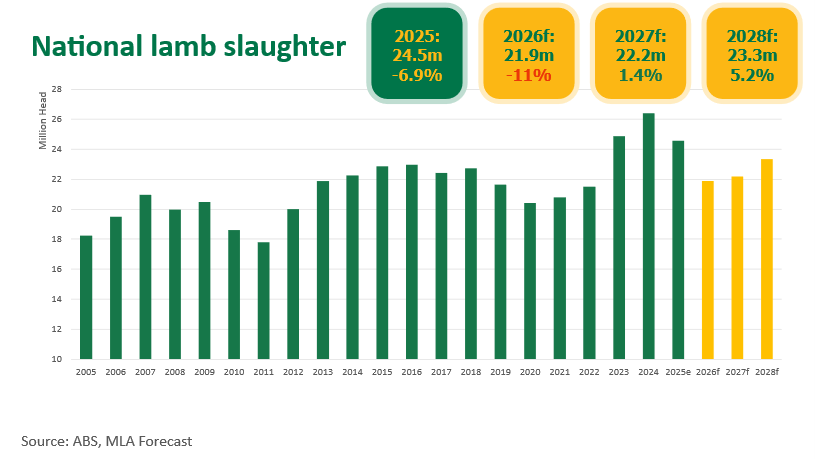

羔羊及绵羊屠宰量回落,将进一步收紧市场供应。

饲料管理、种羊留存及企业经营灵活性,将成为 2026 年行业发展的关键要素。

澳大利亚绵羊产业步入 2026 年,整体供应趋紧、种群调节空间收窄,南部主产区尤为明显。全国绵羊存栏量预计下降 2.7%,降至 6710 万只,凸显气候环境持续承压,且多年来出栏量居高不下的现状。

对养殖从业者而言,核心结论是:短期内羊群复产扩容的选择空间大概率持续受限。

维多利亚州、南澳、塔斯马尼亚以及新南威尔士州南部的干旱天气,持续制约牧草供给、饲草储备并打压行业养殖信心。尽管部分地区近期降雨带来一定缓解,但多数养殖户在存栏规模、种畜留存及补群更替决策上仍保持谨慎。

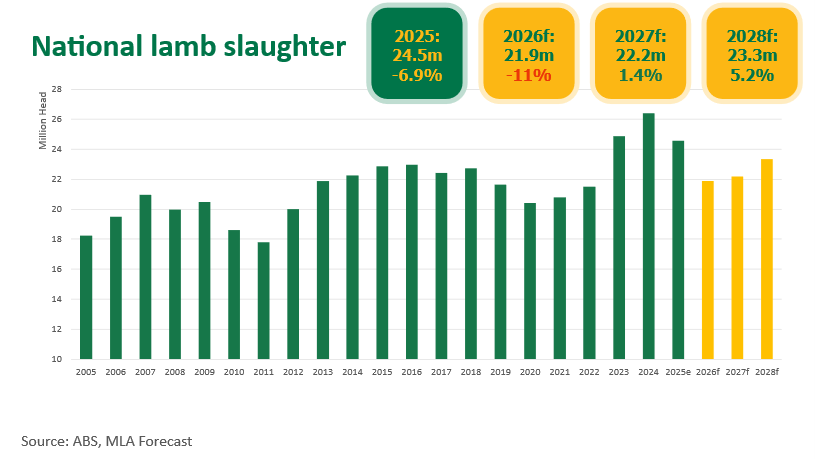

这份谨慎态度也体现在 2026 年屠宰量预期中。预计羔羊屠宰量下滑 11%,至 2186 万只;成年绵羊屠宰量降幅达 30%,降至 713 万只。这意味着可上市畜源进一步缩减,羊群复产进程也将放缓。近年包括繁育母羊在内的大量出栏抛售,已削弱行业短期内扩充存栏的能力。

落到牧场经营层面,羊群养殖决策将完全取决于气候饲草形势的向好预期。饲料供给紧张的养殖户,或将权衡选择留存种羊、提前出栏,或是调整养殖结构,以此管控经营风险与现金流压力。多数产区要实现实质性的羊群规模恢复,仍需等待饲草条件出现大范围、持续性的好转。

尽管屠宰量有所下降,但依托胴体平均重量持续提升,整体产量仍有望保持相对韧性。预计羔羊产量小幅回落 10%,至 53.7 万吨胴体重;羊肉产量下滑 29%,至 18.477 万吨胴体重。这凸显出在存栏数量收紧时,育肥体系维持生产性能的重要价值。品种基因改良、谷物饲喂、舍饲养殖模式的持续完善,以及市场对大体重羔羊的需求,将继续支撑这一趋势。

羊毛也重新成为养殖生产布局中的重要一环。羊毛价格走强提升了美利奴羊养殖收益,有望推动养殖户在条件允许情况下选择留存存栏。未来 12 个月,对于美利奴牧场及混业养殖主体而言,这一变化或将持续影响羊群结构调整与种畜留存决策。

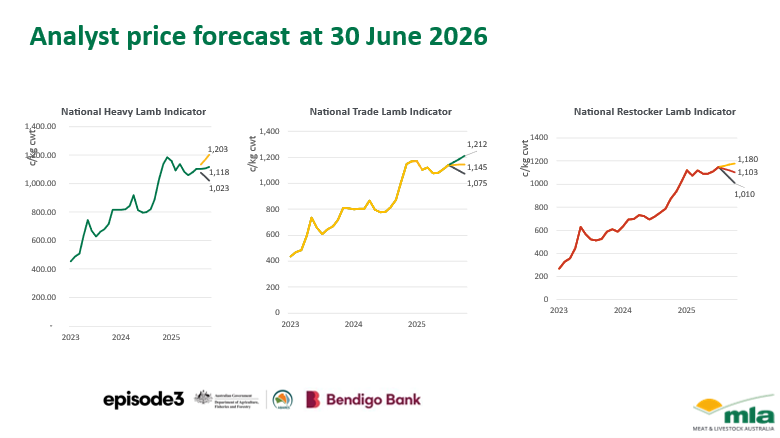

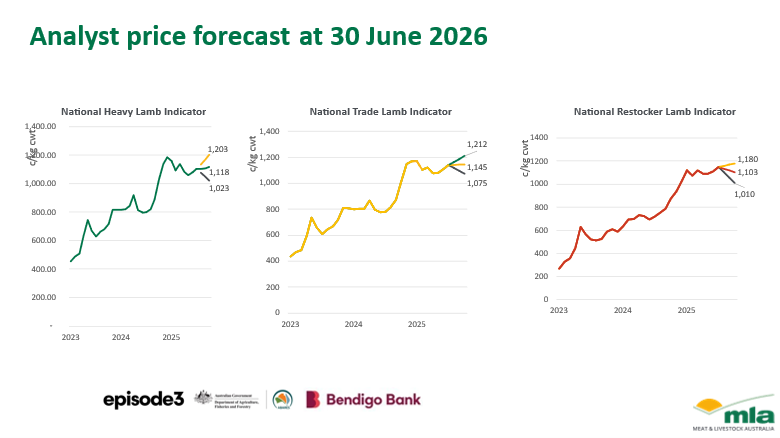

育肥羔羊价格预计维持坚挺,但若气候饲草形势持续分化,补栏引种需求或将持续偏弱。行业展望显示,2026 年经营管理的重要性将与市场行情走势同等关键。做好饲料预算、保住核心种畜、紧盯出栏体重与市场规格标准,会比盲目追求养殖规模更为重要。

总体来看,2026 年重在守住经营弹性。绵羊存栏收紧叠加气候条件参差不齐,将使种群复产决策保持谨慎;而育肥成品市场行情向好,将持续回馈增重出栏、择机上市、达标合规的经营模式。能够精细管控饲料、留存优质繁育母羊、稳定育肥出栏水平的养殖主体,待气候与行业景气度回升时,将更具应变与发展优势。

消息来源:MLA

Smaller flock sharpens shift in production focuses

Key points

The national sheep flock is forecast to fall to 67.1 million head in 2026.

Lower lamb and sheep slaughter will tighten supply.

Feed management, breeder retention and enterprise flexibility are shaping up to be critical for 2026.

Australia’s sheep industry is heading into 2026 with tighter supply and reduced flock-level flexibility, particularly across southern production regions. The national flock is forecast to decline 2.7% to 67.1 million head, reflecting ongoing seasonal pressure and several years of elevated turn-off.

For producers, the key takeaway is that rebuild options are likely to remain limited in the short-term.

Dry conditions across Victoria, SA, Tasmania and southern NSW continue to weigh on pasture availability, fodder reserves and confidence. While recent rainfall has offered some relief in parts, many producers remain cautious around stocking rates, retention and replacement decisions.

This caution is reflected in the 2026 slaughter outlook. Lamb slaughter is forecast to fall 11% to 21.86 million head, while sheep slaughter is forecast to decline 30% to 7.13 million head. This points to a smaller pool of available stock and a slower pathway to rebuilding. Heavy turn-off in recent years – including breeding females – has reduced the industry’s immediate ability to lift numbers.

On farm, this means flock decisions will hinge on seasonal confidence. Producers with tight feed supply may weigh up whether to retain breeders, sell earlier, or adjust their enterprise mix to manage risk and cash flow. In many regions, meaningful flock rebuilding is unlikely until feed conditions improve more broadly and consistently.

Production is expected to remain relatively resilient despite reduced slaughter, supported by continued gains in average carcase weights. Lamb production is forecast to ease 10% to 537,000 tonnes carcase weight (cwt), while mutton production is expected to fall 29% to 184,770 tonnes cwt. This underscores the value of finishing systems that maintain performance when numbers tighten. Ongoing improvements in genetics, grain feeding, containment feeding and demand for heavier lambs will continue to support this trend.

Wool is also re-emerging as an important part of the production equation. Stronger wool prices are improving returns from Merino enterprises, potentially encouraging producers to retain sheep where conditions allow. For Merino and mixed-enterprise operations, this shift could increasingly influence flock structure and retention decisions over the next 12 months.

Finished lamb prices are expected to remain firm, though restocker demand may stay softer if seasonal conditions remain uneven. The outlook suggests 2026 will be a year where management matters as much as market direction. Feed budgeting, protecting core breeders and targeting weight and market specifications are likely to be more important than chasing volume.

Overall, 2026 is shaping up as a year to protect flexibility. Tighter sheep numbers and mixed seasonal conditions are likely to keep rebuild decisions cautious, while strong finished markets continue to reward weight, timing and meeting specification. Businesses that manage feed carefully, retain productive breeders and maintain finishing performance are likely to be better placed to respond when seasonal confidence lifts.

Source:MLA