核心要点

维多利亚州与南澳州的季节性条件持续改善,进一步提振补栏养殖户信心。

线上羔羊价格指数上周创下历史新高。

除杜泊羊外,所有品种羔羊售价均超过200澳元/头。

季节性条件改善与供应紧张,共同支撑补栏需求。

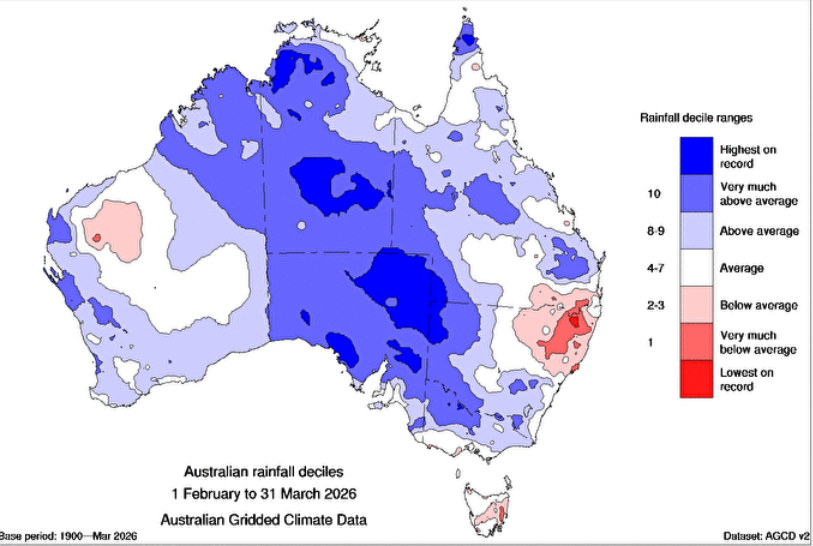

年初以来气候条件向好,大幅提振了澳大利亚南部地区的羔羊补栏需求。维多利亚州部分地区录得有记录以来最湿润的二至三月,州内西部地区表现尤为突出;南澳州南部区域也持续迎来有效降雨。近几周接连的降雨天气进一步巩固了土壤墒情、提升牧草供给,养殖生产环境得到显著改善。

2026 年 2-3 月澳大利亚降水量十分位图。来源:澳大利亚气象局。

这些有利气候条件,正叠加在本已偏紧的供给背景之上。预计全国羊群存栏量将在2028年降至6400 万头的历史低位,供给受限进一步加剧了加工企业、育肥场与补栏养殖户之间的竞争。因此,价格走强不仅源于供给稀缺,也越来越受到生产前景信心的支撑。

线上交易指标创历史新高

这份信心在线上补栏市场中体现得尤为明显。MLA 的线上羔羊指标(通过数字平台追踪补栏交易活跃度)在截至4月12日的当周飙升至历史新高226.90澳元/头,当周成交量约16.9万头羔羊。这一价格水平反映出,受牧草条件改善和中期前景向好的支撑,养殖户重启或扩大养羊业务的意愿十分强烈。

需求的强劲势头已从羔羊延伸至种羊市场。线上绵羊指标在3月底创下历史新高331.65澳元/头,尽管对应交易量较小。尽管近几周价格略有回落,但仍处于历史高位,表明市场对重建母羊存栏基数的兴趣持续存在。

地区与品种趋势反映季节性气候条件

地理层面上,需求主要由季节性条件优越、饲草充足的地区推动。来自马利、里弗赖纳、新南威尔士州中西部,以及南澳州墨累 - 达令盆地的羔羊,正受到最激烈的竞争。相比之下,来自新南威尔士州西部和西北部、北部高地以及昆士兰州部分河道地带等干旱地区的羔羊,补栏需求则较为疲软,凸显了季节性条件与采购行为之间的明确关联。

线上平台的品种表现进一步印证了市场的强劲态势。美利奴羊、萨福克羊、杂交羊、无角陶赛特羊和边区莱斯特羊等多数主要品种,交易均价均稳定维持在200澳元/头以上。近期唯一跌破这一水平的品种是杜泊羊,其当周价格下跌了16澳元/头。

实体销售与买家结构变化支撑市场动能

线上交易活跃度的激增反映了更广泛的市场趋势,并在实体拍卖市场中得到印证。过去一年里,补栏羔羊指标上涨了约42澳分/公斤(涨幅近10%),同期美利奴羔羊指标上涨了约44澳分/公斤。

展望未来,买家需求结构可能发生变化。受谷物价格上涨、种植面积减少影响,育肥场买家的活跃度预计将有所下降,养殖经济效益正重新向牧草育肥模式倾斜。同时,受羊毛价格回升带动,美利奴羊的需求也重回上升通道。

总体而言,当前市场动态是供给偏紧、季节性条件改善和养羊业信心增强三者共同作用的结果。线上补栏需求的强劲表现,不仅支撑着价格水平,也传递出养殖户重建羊群的明确意愿。

内容出处:市场信息部经理 斯蒂芬·比格内尔

信息截至2026年4月16日撰稿时准确有效。

澳大利亚肉类与畜牧业协会不对本刊物所载任何信息的准确性、完整性及时效性作出任何保证。使用者自行承担使用或采信本刊物内容所产生的全部风险,对于因相关使用或采信行为造成的任何损失及损害,协会不承担任何责任。未经协会事先书面许可,本刊物任何内容不得转载复制。凡使用协会刊物、报告及相关信息,均须遵守其市场报告与信息使用条款。

消息来源:MLA

Restocker confidence builds as Online Lamb Indicator hits record highs

Key points

Seasonal conditions in Victoria and SA are improving, boosting restocker confidence.

The Online Lamb Indicator reached a record high last week.

All breeds except Dorpers are fetching over $200/head.

Seasonal conditions and tight supply underpin restocker demand

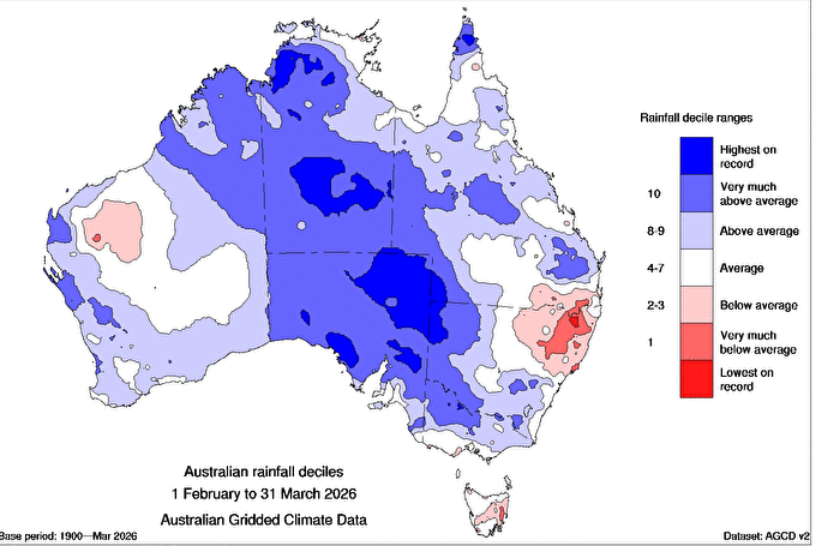

Favourable seasonal conditions since the start of the year have underpinned a sharp lift in restocker demand, particularly across southern Australia. Parts of Victoria recorded their wettest February–March period on record, especially in the state’s west, while southern regions of SA have also benefited from consistent rainfall. Follow-up fronts in recent weeks have reinforced soil moisture and pasture availability, setting up a markedly improved production environment.

Australian rainfall deciles for Feb-Mar 2026. Source: Bureau of Meteorology.

These conditions are coinciding with an already-tight supply backdrop. The national flock is projected to hit a record low level of 64 million head in 2028, and this constrained supply is intensifying competition across processors, feeders and restockers. As a result, pricing strength is being driven not just by scarcity, but increasingly by confidence in the production outlook.

Online indicators reach record highs

This confidence is particularly evident in online restocker markets. MLA’s Online Lamb Indicator, which tracks restocker activity through digital platforms, recently surged to a record $226.90/head in the week ending 12 April, with approximately 169,000 lambs transacted. This level of pricing reflects strong intent from producers to re-enter or expand sheep operations, supported by improving pasture conditions and a more positive medium-term outlook.

The strength in demand extends beyond lambs into breeding stock. The Online Sheep Indicator reached an all-time high of $331.65/head at the end of March, albeit across a smaller offering. While prices have eased slightly in recent weeks, they remain historically elevated, indicating sustained interest in rebuilding ewe bases.

Regional and breed trends reflect seasonal conditions

Geographically, demand is being driven by regions with strong seasonal conditions and feed availability. Lambs sourced from the Mallee, Riverina, Central West NSW and the Murray–Darling Basin in SA are attracting the strongest competition. In contrast, offerings from drier regions such as western and north-west NSW, the Northern Tablelands and parts of Queensland’s Channel Country are seeing softer restocker interest, highlighting the clear link between seasonal conditions and buying behaviour.

Breed performance on online platforms further reinforces the strength of the market. Most major breeds – including Merinos, Suffolks, crossbreds, Poll Dorsets and Border Leicesters – are consistently trading above $200/head. The only segment to dip below this level recently has been Dorpers, which have eased $16/head this week.

Momentum supported by physical sales and shifting buyer dynamics

The surge in online activity is indicative of broader trends and is being mirrored in physical saleyards. Over the past year, the Restocker Lamb Indicator has lifted by approximately 42¢/kg (just under 10%), while the Merino Lamb Indicator has risen by around 44¢/kg over the same period.

Looking ahead, the composition of buyer demand may evolve. Feedlot buyers are expected to be somewhat less active, as higher grain prices and reduced planting areas shift the economics back towards pasture-based finishing systems. Merinos are also back in demand due to improving wool prices.

Overall, the current market dynamic reflects a convergence of tight supply, improved seasonal conditions and growing confidence in the sheep sector. The strength in online restocker demand is not only supporting prices but also signalling interest from producers to rebuild their flocks.

Attribute content to: Stephen Bignell, Manager – Market Information

Information is correct at time of writing on 16 April 2026.

MLA makes no representations as to the accuracy, completeness or currency of any information contained in this publication. Your use of, or reliance on, any content is entirely at your own risk and MLA accepts no liability for any losses or damages incurred by you as a result of that use or reliance. No part of this publication may be reproduced without the prior written consent of MLA. All use of MLA publications, reports and information is subject to MLA’s Market Report and Information Terms of Use.

Source:MLA